Before we get started, I want to briefly outline the main topics covered in this post by answering the following questions:

- What are the differences between A-income and B-income?

- What are Personal Income and Shares Income and how are they calculated?

- What is Top-bracket tax (Topskat) and when one must pay it?

- What are the differences between RSUs and ESPP and what type of tax one should pay for each?

Introduction

I will describe the high level of what kind of tax one must pay for RSUs and ESPP. This is documented based on my own experience, and not everything might be 100% accurate. It follows the Danish taxation rules and it doesn’t consider cases where double taxation applies (when you have to pay taxes in your home country as well), so read more about the individual double taxation agreements on the website of the Danish Ministry of Taxation here.

To understand why one might need to calculate how much they owe SKAT, there is a distinction I want to mention in regards to compensation. When an employee is compensated with both salary and equity (stocks), the employer reports both compensations to SKAT, but this income is taxed differently:

- The salary is reported as A-income (A-indkomst) on which tax is withheld before payment.

- The equity is reported as B-income (B-indkomst) on which no tax is withheld when they are paid. In other words, you need to voluntarily pay the tax for this type of income.

If you ask: “What will happen if I don’t pay my outstanding tax by the end of December, and I pay it in March?” The answer is simple. You will be charged interest on a daily basis at an annual rate of 1.8% from 1 January until the day when you make the payment. So if you are ok with paying that, you can skip all these calculations and wait for SKAT to ask you for money in March. (Please note that if you decide to sell any of the stocks, then you will need to report them, so SKAT knows how to calculate gains/losses. You can read more about this below)

For example, if you have to pay DKK 100.000 back to SKAT and you pay in March, you will have to pay an extra of DKK ~400.

How to find reported income

You can find what your company already reported to SKAT by logging in skat.dk and navigating as follows:

Skatteoplysninger > Se personlige skatteoplysninger > 2021 (or any other year you are interested)

Then you must look for the section called ‘Arbejdsgiver’ under which your company name is listed. Here you will see field 13 (A-indkomst) and field 36 (B-indkomst).

(Please note that these are taxable amounts, and NOT what you owe SKAT)

What are RSUs and ESPP?

Restricted Stock Units (RSUs) are a form of compensation companies give to their employees in the form of company shares. RSUs are restricted during a vesting period that may last several years, during which time they cannot be sold. Once they vest they are just like any other shares of company stock. Their value is considered income once vested.

An employee stock purchase plan (ESPP) is a company-run program in which employees contribute through salary deduction and can purchase company stock at a discounted price. The gain between the purchase price and the fair market value is considered personal income.

Once one sells any of the owned shares, the profit is considered shares income.

Types of taxation

Before we dive into what kind of tax one must pay, I will describe some details about the different types of taxation I will mention in this post.

For both RSUs and ESPP (at some point) one will pay two types of taxes. The two types are personal income (Personlig indkomst) and shares income (Aktieindkomst).

Personal income tax

This tax percentage can vary from case to case, but in general, it is based on the following:

- 8% Labour market contributions (AM-bidrag/Arbejdsmarkedsbidrag)

- 12,09% Bottom-bracket tax (Bundskat)

- 23,8% Municipal tax (Kommuneskat) – Copenhagen municipality

- Each municipality has its own tax, find yours here

- 0,8% Church tax (Kirkeskat) – Copenhagen municipality

- Each municipality has its own church tax, find yours here

- 15% Top-bracket tax (Topskat)

- This is only paid if one has an income over DKK 544.800/year (as of 2021) after deduction of labour market contributions or a salary of apx. DKK 49.000/month before tax. (See examples below)

Let’s take a few examples and go through them step by step and see how each percentage is calculated.

Example 1

Let’s take an example of a salary below the Top-bracket tax limit and an extra B-income that will cross the Top-bracket limit. In other words, if one was not to get the extra B-income, they wouldn’t have to pay Top-bracket tax. (For the sake of simplicity, will not apply Church tax and will use Copenhagen’s municipality tax rate)

Salary: DKK 540.000 (DKK 45.000/month)

B-income: DKK 100.000 (Let’s say from RSUs)

Total income: DKK 640.000

Step 1 (Deduct Labour market contributions)

8% of DKK 640.000 = DKK 51.200

Amount after deduction = 640.000 – 51.200 = DKK 588.800

Step 2 (Deduct Bottom-bracket tax)

12,09% of DKK 588.800 = DKK 71.185,92

Step 3 (Calculate personal deductions)

Before deducting the Municipality tax, one needs to calculate the personal deductions. This can vary from case to case, but some general deductions are Employment allowance (DKK 40.600), Job allowance (DKK 2.600), Pension allowance (up to DKK 8.964 <> 12% on contributions up to DKK 74.700), etc. For the sake of simplicity, in this example will only deduct the Employment and Job allowances.

Personal deductions = DKK 43.200 (DKK 40.600 + DKK 2.600)

Step 4 (Deduct Municipality tax)

Before applying the Municipality tax, one must calculate the taxable amount. To the total income after labour market contributions, we add/subtract gains/losses from Income from capital (Kapitalindkomst; more about this in a following post) and subtract the personal deductions. To keep it simple, we will not use any Income from capital in this example.

23,8% of DKK 545.600 (588.800 – 43.200) = DKK 129.852,8

Step 5 (Deduct Top-bracket tax)

As we mentioned above, everything above the limit (544.800) after the Labour market contributions (588.888), is taxed with an extra of 15%.

15% of DKK 44.088 (588.888 – 544.800) = DKK 6.613,2

Finally, we sum together the amounts

DKK 51.200 (Labour market contributions)

+ DKK 71.185,92 (Bottom-bracket tax)

+ DKK 129.852,8 (Municipality tax)

+ DKK 6.613,2 (Top-bracket tax)

————————

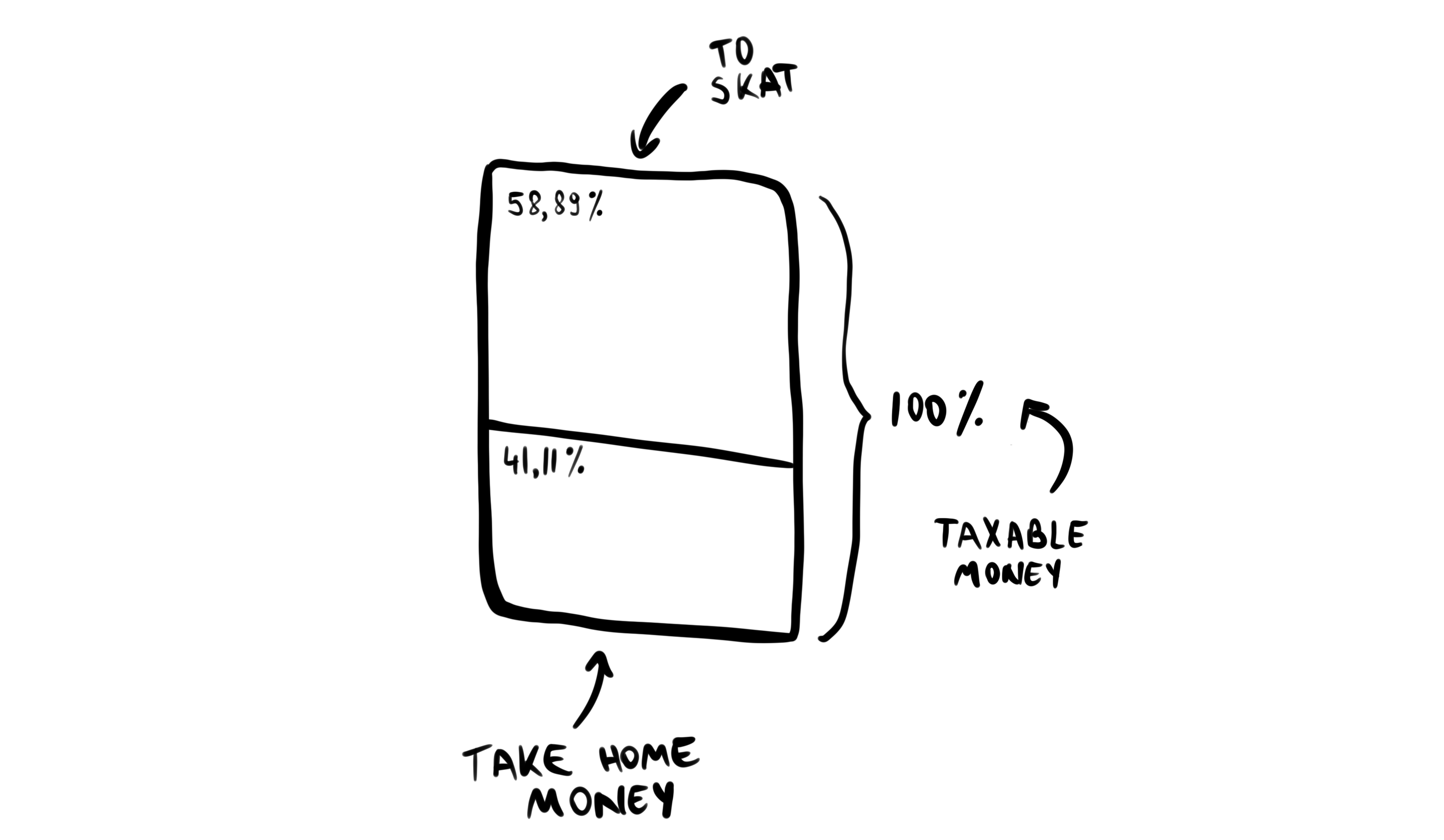

= DKK 258.851,92 (~40,44%)

Please note that this amount is just the tax owed for the personal income. There are other allowances that could be applied (Personal allowance, deductions for interest expenses, etc.), but that is beyond the scope of this example.

Example 2

Let’s take an example of a salary below the Top-bracket tax limit and an extra B-income that will not cross the Top-bracket limit. (For the sake of simplicity, will not apply Church tax and will use Copenhagen’s municipality tax rate)

Salary: DKK 480.000 (DKK 45.000/month)

B-income: DKK 100.000 (Let’s say from RSUs)

Total income: DKK 580.000

Step 1 (Deduct Labour market contributions)

8% of DKK 580.000 = DKK 46.400

Amount after deduction = 580.000 – 46.400 = DKK 533.600

Step 2 (Deduct Bottom-bracket tax)

12,09% of DKK 533.600 = DKK 64.512,24

Step 3 (Calculate personal deductions)

We will use the same personal allowances from the previous example

Personal deductions = DKK 43.200 (DKK 40.600 + DKK 2.600)

Step 4 (Deduct Municipality tax)

23,8% of DKK 490.400 (533.600 – 43.200) = DKK 116.715,2

Step 5 (Deduct Top-bracket tax)

The Top-bracket tax is 0%, because the amount after labour market contributions is below the tax limit (DKK 533.600 < DKK 544.800)

Finally, we sum together the amounts

DKK 46.400 (Labour market contributions)

+ DKK 64.512,24 (Bottom-bracket tax)

+ DKK 116.715,2 (Municipality tax)

———————–

= DKK 227.627,44 (~39.24%)

Example 3

For this example, we will use a salary above the Top-bracket tax limit with an extra B-income. (For the sake of simplicity, will not apply Church tax and will use Copenhagen’s municipality tax rate)

Salary: DKK 660.000 (DKK 55.000/month)

B-income: DKK 100.000 (Let’s say from RSUs)

In general, we don’t need to calculate the taxes paid for the salary, because that is done by SKAT already, so let’s focus on calculating the tax only for the B-income amount.

Step 1 (Deduct Labour market contributions)

8% of DKK 100.000 = DKK 8.000

Amount after deduction = 100.000 – 8.000 = DKK 92.000

Step 2 (Deduct Bottom-bracket, Municipality and Top-bracket tax)

50,89% (12,09% + 23,8% + 15%) of DKK 92.000 = DKK 46.818,8

Note: We assume the personal allowances were deducted when calculating the salary.

Finally, we sum together the amounts

DKK 8.000 (Labour market contributions)

+ DKK 46.818,8 (Bottom & Top brackets and Municipality tax)

———————

= DKK 54.818,8

That’s roughly ~54,82% tax on personal income from RSUs. Crazy ah?

Note: There is a Tax ceiling for personal income (Skatteloft – personlig indkomst) of 52,06 % (as of 2021). This means that if one’s personal income tax (without AM-bidrag) exceeds 52,06%, one will get a deduction on the topskat paid amount. Let’s take Hvidovre as an example: For a tax of 52,59% (= 12,09% + 25,5% + 15%), you will get a 0,53% deduction.

Shares income tax

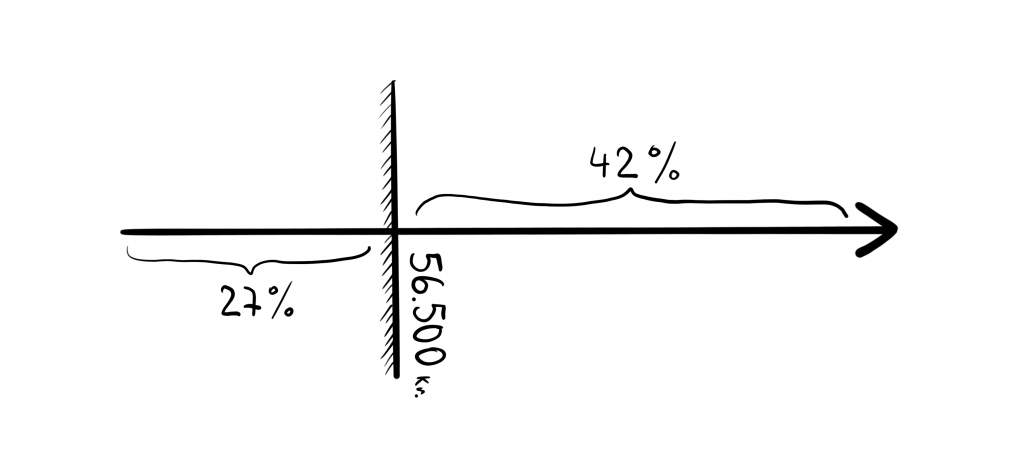

This tax calculation is pretty simple. As of 2021, it has a progression limit (progressionsgrænse) of DKK 56.500. Whatever is below that limit is taxed with 27%, and everything above the limit is taxed with 42%. The progression limit doubles to DKK 113.000 if you are married.

Example

For a shares income of DKK 80.000

27% of DKK 56.500 = DKK 15.255

42% of DKK 23.500 (80.000 – 56.500) = DKK 9.870

Total = DKK 25.125 (~31,4%)

Taxation of RSUs

Because RSUs are given by companies for free, the employee has to pay personal income tax on the entire amount at the vesting time. The amount is calculated by multiplying the number of shares x Purchase Fair Market Value (FMV).

Let’s take an example: If I receive a number of 10 shares, at the FMV price of $100, then my taxable amount will be $1000 (10 x 100). In other words, I will have to pay $548,2 (which is 54,82% x $1000).

Taxation of ESPP

Compared to the RSUs, we don’t need to pay taxes for the entire amount and that is because we already paid for a part of it when we received our salary. To keep it simple, we will only exemplify using the purchase price and the purchase FMV.

Purchase price = The price one pays for a share, after calculating the lowest buying price and applying the employee deduction.

Purchase FMV = The price the share is worth on the market at the time of buying.

Let’s take an example: If I buy a number of 100 shares at the purchase price of $50 and the purchase FMV price of $100, to calculate the taxable amount we need the total purchase value and the total market value based on the purchase FMV. In other words, we don’t pay taxes on what we paid already (as we paid tax when we got our salary), and only pay on the realized gains.

Total market value = shares x purchase FMV (what is worth on the market)

Total purchase value = shares x purchase price (what one paid already)

Taxable amount = total market value – total purchase value (the amount one needs to pay tax for)

Taxable amount = 100 x $100 – 100 x $50 = $5000

Now that we have the taxable amount ($5000) and we also know the personal income percentage (54,82%), we can calculate the tax amount one needs to pay:

Tax amount = $5000 x 54,82% = $2741

Taxation on share gains

When selling shares, any profit is considered shares income (Aktieindkomst). Basically, we need to apply to the taxable amount the ‘shares income tax’ described above.

To calculate the taxable amount, we need to keep in mind two things: The average cost method and the FIFO principle (First In First Out). In a following post I will describe in detail how to calculate this taxable amount, so stay tuned!

For SKAT to know how to calculate the gains/losses when we sell shares, they need to be reported in the Stocks inventory. Some companies will report the shares when you receive (buy) them, but in general, you will have to report both when you buy and sell shares. I wrote a guide in my other post here.

Conclusion

- Equity (stocks) compensation tax has to be paid voluntarily.

- When your RSUs vest and when you buy shares within ESPP, you pay personal income tax.

- When you sell any of the shares, you pay shares income tax.

- If you don’t pay your B-income tax before the end of the calendar year, you will be charged interest until you pay the outstanding tax.

Do you have any questions? Feel free to drop a comment below!

Further reading:

Restricted Stock Unit (RSU)

Employee Stock Purchase Plan (ESPP)

Tax glossary

Tax rates (Danish)

Interest for outstanding tax in 2020

Buying and selling shares and securities

Gain and loss are determined according to the average cost method

Disclaimer: The information presented in this blog post is intended for information and entertainment purposes only and is not meant to be taken as financial advice, legal advice, tax advice or any other kind of direction. You should seek advice from a tax or investment advisor for further guidance.