In this post I’m going to describe the reason one must register their RSUs and ESPP shares into SKAT and also how to do it. We will go through when one needs to report their shares, what it means to have gains/losses and how to register them with examples.

This guide will only work if you had shares reported in the previous taxation year, or if it is already March and you are allowed to correct your annual statement (årsopgørelsen) for the previous year.

Before you start registering your shares into the inventory, ask your company if they already report purchase/sales to SKAT. These are different then RSUs awards and ESPP discounts reported as B-income.

The reason for reporting the shares to SKAT

The only reason one must report their shares bought through RSU or ESPP is so SKAT knows if you have gains or losses after you sold any shares. In other words, if you haven’t sold any shares yet, you don’t have to report them, but will still have to do that once you start selling.

Registering both “purchases” and “sales” of your shares, SKAT will either ask you to pay more tax if you have realized gains, or they will register your losses and you will pay less tax in the following years.

Even if you are not selling in the near future, it is good practice to register your “purchases” as it will make it easier in the future to have your stocks inventory up to date. Then, when you plan on selling, you would only have to go through the registration of those shares, instead of everything.

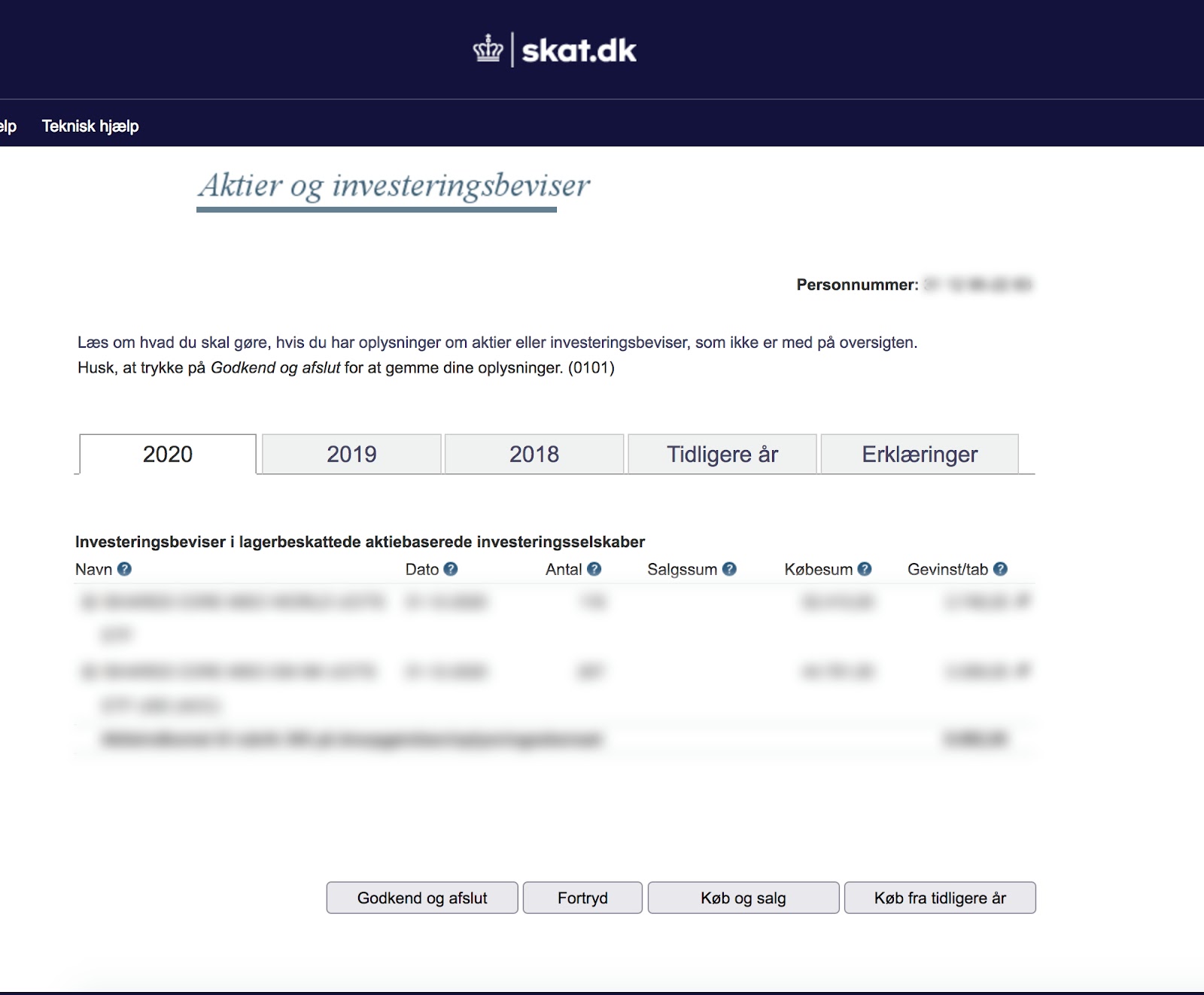

How to get to the stocks inventory

To access the stocks registry, you can navigate from Årsopgørelse > Ret årsopgørelsen and search for Rubrik 345 (or any other stocks related rubrik) and click on the calendar icon (Fig. 1). Another way is to directly access this link. Once you get to the inventory, you will see something similar to Fig. 2 if you have other registered shares, or an empty page.

How to register the stocks into the inventory

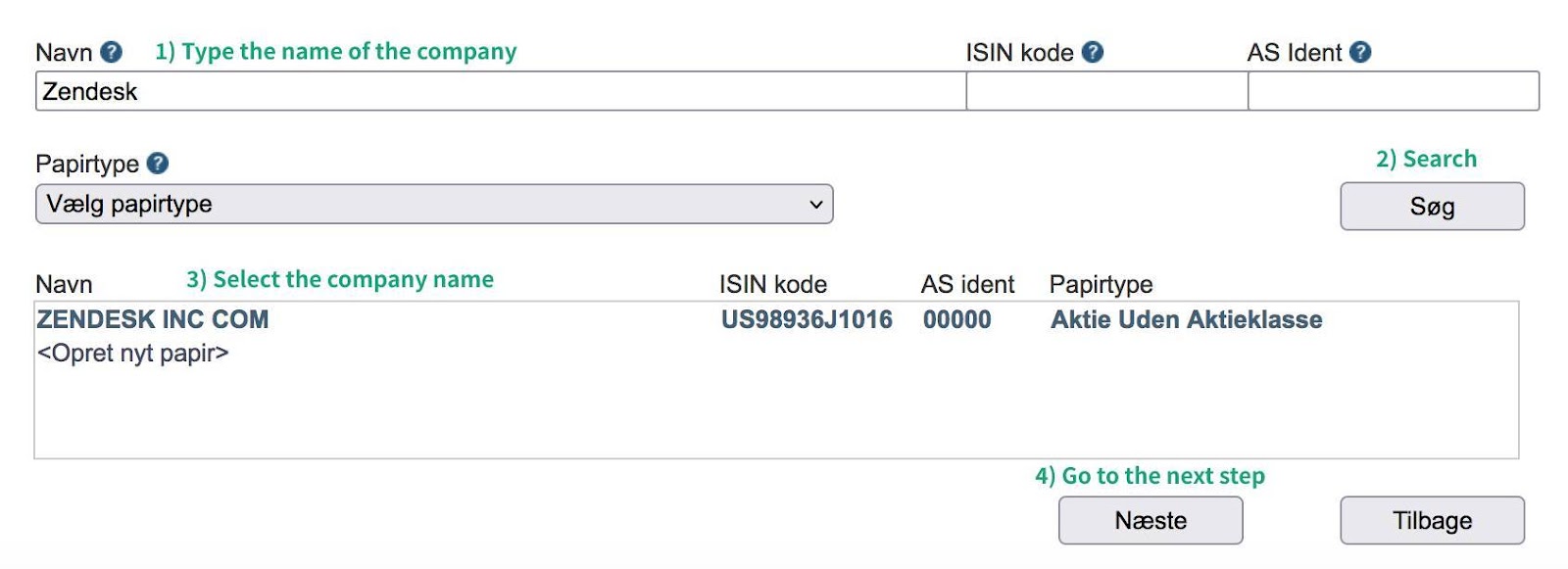

The easiest way to find your company for which you want to register the stocks is to use the search by name functionality as shown in Fig 3.

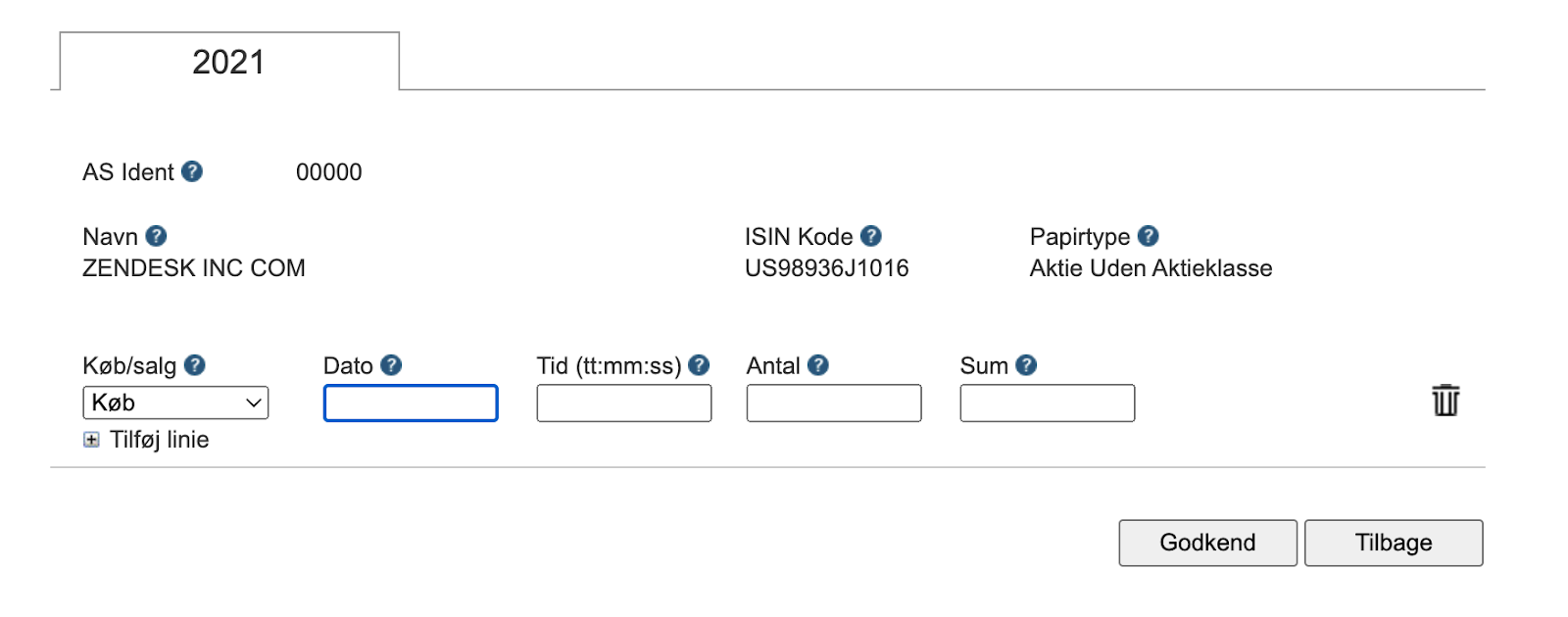

Once that is done, then you can add shares you bought or sold. The information needed is described as follows:

- Dato: The date in DD-MM-YYYY format

- Tid (tt:mm:ss): The precise time is not very important, unless there were more purchases/sales in the same day. Because of the average cost method and the FIFO principle (First In First Out), it is important to register them in the exact order. If there were 3 sales in one day, selecting 1pm for the first sale, 2pm for the second, etc. will be enough to register them in the right order.

- Antal: The number of shares

- Sum: The total amount in DKK. This amount will represent different prices for RSUs vs ESPP. Read more below

The purchase price

There is an important difference between RSU and ESPP when reporting the purchase price. For the RSU, the purchase price is the same as the purchase Fair Market Value (FMV), so your price per share is the purchase FMV. In other words, because the RSUs are awarded to you for free by your company, you report the FMV price you get them at.

On the other hand, for ESPP, your purchase price will be different from the purchase FMV. The reason for that is that you contribute with your own money for some of the shares value. The question is: Which price do you use, and why? I describe in Taxation of ESPP in more detail what the two prices mean. In that example, we calculate how much tax we pay for the amount between the price we purchased the ESPP and the purchase FMV, which is the discount the ESPP is giving. In other words, we already paid for the difference between the two prices (Your company reported that amount to SKAT as B-income, read more in this post)

Now, if we use the purchase price, we will pay double tax for the discounted amount we gain from our ESPP. Therefore, we should always report the purchase FMV for ESPP.

In summary, we should always use the purchase FMV value for both RSUs and ESPP.

Gains and losses

Let’s say we buy 10 shares at $100 per share. For SKAT to know if we made a profit/gain or had a loss when we sold our shares, we need to report it.

In our example, let’s say we sell the 10 shares with $80 per share. In this case, we are having a loss: 10 x $80 – 10 x $100 = -$200. SKAT will then ask us for less money if we owe any this year, else, in the following year(s) we will be asked to pay less because of the loss we had this year.

On the other hand, if we sell our 10 shares at 150$ per share, in this case, we are making a profit: 10 x $150 – 10 x $100 = $500. SKAT will then ask us for more money in tax.

This is why it is important to report purchases/sales.

Stocks inventory template

To make it easier and have all the needed data before entering the purchases/sales into SKAT’s inventory, I use a simple excel template where I register all the transactions. You can find the template here with some examples. In this template, I also do the currency conversions from USD to DKK, as we need to enter the values in DKK. If you need to convert from a different currency into DKK, make sure you update the template and also use the right exchange rates from the Danish National Bank. Please be aware that the data from the National Bank is per 100 units currency. For example, for the date of 14th of March, 2022 the exchange rate for 100 USD dollars is 678.88, meaning the rate for one USD to DKK is 6.7888

For the ESPP, in general you will see the exchange rate on the statement from your broker. Because you use DKK to buy shares, the conversion goes the other way around: DKKUSD. Make sure to use that rate instead, and for RSUs and when selling, use the rates for USDDKK from linked above.

Conclusion

- Ask your company if they report purchases/sales to SKAT to avoid duplicates of shares in the inventory, and if they don’t report them, you need to manually register them into the Stocks Inventory.

- Even if your company reports RSUs and the ESPP discount as B-Income, you still need to register your purchases/sales to calculate gains/losses.

- Always use the Purchase FMV when reporting RSUs and ESPP shares.

- Convert the amounts to DKK before registering the transactions in the inventory.

- If there are multiple sales in the same day, update the time so they follow the right order.

Do you have any questions? Feel free to drop a comment below!

Disclaimer: The information presented in this blog post is intended for information and entertainment purposes only and is not meant to be taken as financial advice, legal advice, tax advice or any other kind of direction. You should seek advice from a tax or investment advisor for further guidance.

This is so extremely helpful and clearly structured. Thanks for sharing your insights!

Really good article! Thanks for sharing your experience. One question: The stock inventory I see seems to be only for stocks in Danish brokers (after I add the stock purchases/sales, it asks me to add the calculated profit in field 66). But stock gains in a US account need to be put into field 454, not 66. Field 454 doesn’t have a stock inventory though. When you click on the calculator on field 454, you’re supposed to add your total net profit per country. Do you know if this means that adding each purchase and sale, while helpful, is not mandatory for US stocks, but it is enough to enter the net profit in 454?

Hey Carl,

This is a tricky one.

It is true that field 454 is for gains and losses on listed foreign shares in foreign deposits. My understanding is that this field should be filled based on account statements from foreign brokers (so you don’t do the calculations manually), as they will not report to SKAT. This case works just fine if you individually buy stock in foreign deposits.

Even tho this is correct, there is an edge-case and that is when you buy (receive RSUs through vesting, or purchase via ESPP) from your company. As far as I know, as of 2019, companies operating in Denmark are required to report employee share purchases, so these shares will show up in the Stocks inventory. That’s why when adding your sales, they will be reported in field 66.

I would not worry too much about this, as regardless of which field (66 or 454), the tax applied to the gains is 27%/42% with the progression rate. I also get the same reporting into field 66.

I want to write SKAT and ask about this edge-case. Since they require companies to report employee shares, it doesn’t really make sense to divide them like that, considering they get reported in field 66 even for foreign deposits. I will get back if I find anything new from SKAT.

I hope this helps,

Dan

Oh, I was wondering about this too at some point and I think you explained it very well! Thanks for sharing all your knowledge on this!